M&A Activity Is Heating Up

M&A Activity Is Heating Up

By: Peter Frerichs

September 2, 2025

Mergers and acquisitions (M&As) are on a hot streak. It’s been an uncertain 2025, but the clouds are parting, and energetic M&A activity is typically a harbinger of economic confidence.

Optimism is high, so much so that even the White House is in on the action, snapping up a 10% stake in Intel.

Public sector moves into private markets are typically reserved for more “socialist leaning” countries, but we’re in unusual political times.

Summer M&A Activity

M&A dealmakers came into the President’s second administration predicting a scorching start. Tariffs dampened expectations, but with the playing field slowly coming into focus, the summer has delivered.

The most hyped deal of the year thus far is Union Pacific’s acquisition of Norfolk Southern for $71.5 billion.[1] M&A activity dealmaking has reached $2.6 trillion globally, driven in large part by U.S.-based megadeals ($10 billion+).[2] While the summer activity is notable, Q1 megadeals really paved the way.

Source: Intellizence. April 8, 2025. “The Largest Mergers & Acquisitions (M&A) Deals - Q1 2025.”

What’s Driving M&A Activity?

Several factors have contributed to the uptick in M&As, but three main drivers stand out:

Interest Rates

The cost of capital matters. In general, more favorable interest rates encourage M&A activity. We are far from the net-zero environment of 2020-2021, but Federal Reserve Chair Jerome Powell’s “strong hint” that interest rate cuts are coming is fueling bullish sentiment for the second half of 2025.[3]

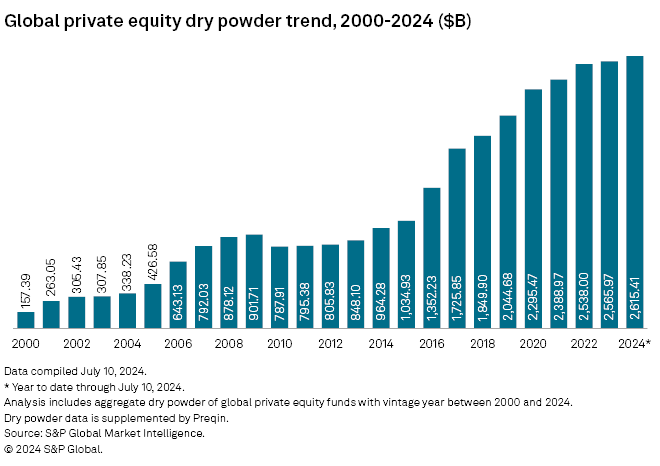

Seller Realism Meets Dry Powder

The gap between buyer appetite and seller valuation expectations widened considerably during the high-interest-rate environment of 2022-2023. Businesses weren’t enthused with buyer offers and relegated themselves to the sidelines. M&A activity slowed, but with global private equity (PE) dry powder at record highs by mid-2024, and more aligned buyer/seller price expectations becoming clearer, an eventual uptick in M&A activity was nearly inevitable.

Over the first half of 2024, global PE and venture capital funds added $49.44 billion to their cash reserves. This alone was more than 1.7 times the $27.97 billion added over the previous 12-month period.[4]

Bullish Bankers

Many of Wall Street’s biggest banks were slashing bonuses by up to 40% in December of 2022. M&A activity had plummeted, leaving banking fees from deal advising through the floor.[5] Fast-forward to the present, and many of those same bankers remember the lean years.

Anu Aiyengar, JPMorgan’s global head of M&A, has been urging her team to seize this favorable climate and finalize deals before the end of the year.[6] Chevron finally closed its $53 billion acquisition of Hess in mid-July, with the banks involved in the deal taking home combined fees of approximately $175 million.[7]

An Eye on ‘95

One of the best runs for the banking industry occurred in 1995 following a series of Fed rate cuts and a favorable law that allowed for bigger bank mergers. The KBW Nasdaq Bank Index, which tracks the 24 largest U.S. banks, culminated the year up over 40%, and over the past 12 months, the index is currently up 32%.[8] Banks are bullish and poised to propel M&A activity over the second half of the year.

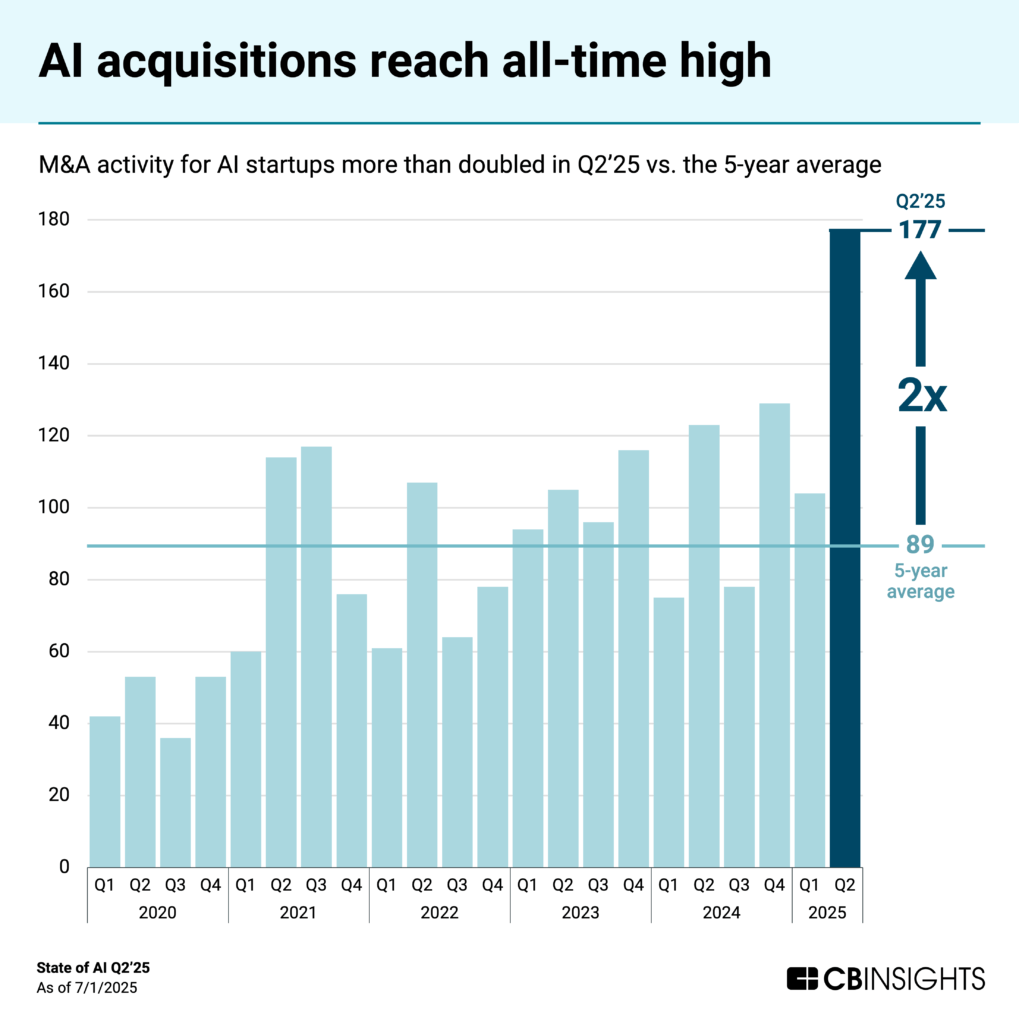

AI’s Role

AI has a role in everything in 2025 - M&A activity is no different. As AI models evolve, many PE funds are employing “AI blueprints” to enhance efficiency across their own operations and those of their portfolio companies. For example, Brookfield, with $150 billion in assets under management, explains that the deployment of customer service AI models across two of its resident infrastructure companies, HomeServe and Enercare, has slashed call times by 15-20% and freed up human assets, resulting in increased sales and customer retention rates.[9]

Second, investment teams are utilizing AI research agents to conduct scenario analyses that leverage historical data from a multitude of previous deals, thereby better preparing research and sales teams. While AI is certainly upending business hiring practices, leaner, more efficient business practices drive M&A activity by allowing a fund’s human assets to take on new business development at a rate that would have been unthinkable without a complementary AI partner.

Source: CB Insights. July 31, 2025. “State of AI Q2’25 Report.”

As expected, M&A activity in AI has surged. IBM acquired three AI companies in Q2, and Intuit, Nvidia, Databricks, and Salesforce all tied for two each.[10]

In addition to traditional M&A activity, big tech is also involved in “quasi-acquisitions.”

- Windsurf - Google hired the company’s R&D employees and executives in a July 2025 $2.4 billion licensing deal.

- Adept - In July 2024, Adept’s founders and a significant portion of its employees were hired by Amazon, while the Seattle behemoth directed over $330 million to license the company’s technology.

- Inflection AI - In a similar deal, Microsoft poached Inflection AI founders and top employees, and paid $650 million in a licensing agreement.

Unlike traditional M&A models, firms like Amazon and Google, through quasi-acquisitions, can be more selective in the talent they onboard and provide startups a path to return capital to their investors via licensing agreements.[11]

Concluding Thoughts

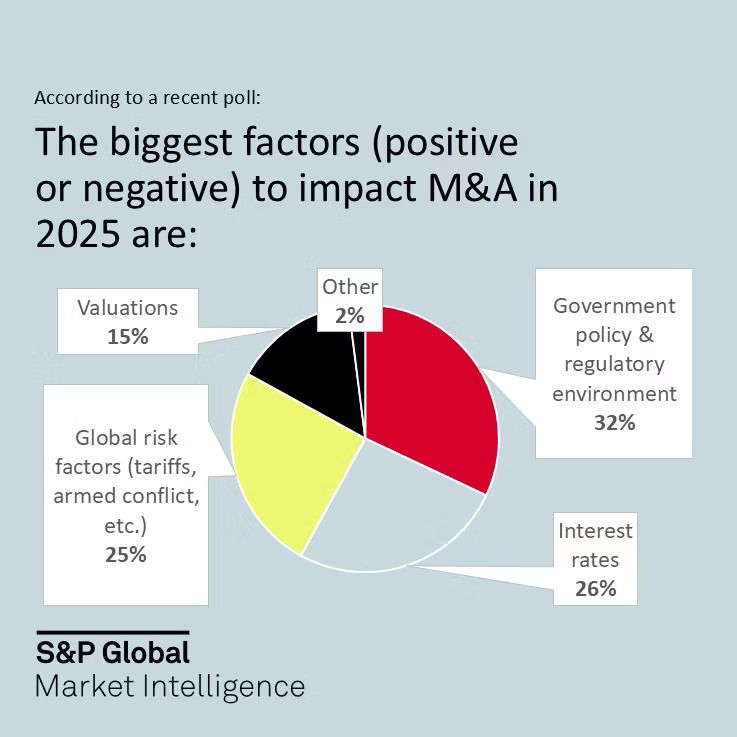

Moving into 2025, polling suggested government policy and the regulatory environment were the biggest factors expected to impact M&A in the new year.

Source: S&P Global. February 4, 2025. “M&A Outlook and Strategic Opportunities in 2025.”

The passage of the “One Big Beautiful Bill” provides corporate America with a 100% bonus depreciation for certain assets and a generous definition of “adjusted taxable income,” among other perks. Through deregulation, the bill also establishes a more favorable M&A environment in sectors such as finance and energy, where regulatory snafus often generate significant dealmaking bottlenecks.

Global risk factors, such as armed conflict, are persistent; however, the tariff regime, although not ideal for some, is clearer. Should interest rates continue to drop, 2025 will shape up to be a banner year for M&As.

Sources:

[1] Isidore, Chris. July 29, 2025. “America’s first transcontinental freight railroad is planned after a megamerger.” CNN Business.

[2] Farr, Emma-Victoria, and Crowley, Amy-Jo. August 5, 2025. “Global M&A hits $2.6 trillion peak year-to-date, boosted by AI and quest for growth.” Reuters.

[3] Bradbury, Rosie. August 22, 2025. “Powell’s hints at rate cuts may energize IPOs, venture debt market.” PitchBook.

[4] Thomas, Dylan, and Sabater, Annie. July 12, 2024. “Private equity dry powder growth accelerated in H1 2024.” S&P Global.

[5] Benoit, David, and Andriotis, AnnaMaria. December 28, 2022. “Wall Street’s Bankers Brace for Big Pay Cuts, but Bosses Don’t Want Whining.” The Wall Street Journal.

[6] Thomas, Laure, and Glickman, Ben. August 3, 2025. “It’s a Scorching Hot Summer for Deals on Wall Street. Vacation Can Wait.” The Wall Street Journal.

[8] Hollerith, David. August 28, 2025. “Big banks are rallying big time. Can it last?” Yahoo Finance.

[9] Janson, Eric. June 24, 2025. “2025 mid-year outlook - Global M&A trends in private equity and principal investors.” PwC.

[10] CB Insights. July 31, 2025. “State of AI Q2’25 Report.”