US Debt - It’s Bad, But We’ve Got Options

US Debt - It's Bad, But We've Got Options

By: Peter Frerichs

July 3, 2025

Insight Highlights

- How we got here and international comparisons

- Elevated debt payments and historical comparisons

- The power of the dollar

- Can we grow our way out of this?

It’s been a busy news cycle. Immigration crackdowns, the Israel/Iran conflict, tariffs - a never-ending barrage of issues are now a daily reality. Yet, one issue that achieves bipartisan consensus, and is equally the fault of both Democrats and Republicans, is the U.S. debt.

The Ugly Reality of the U.S. Debt

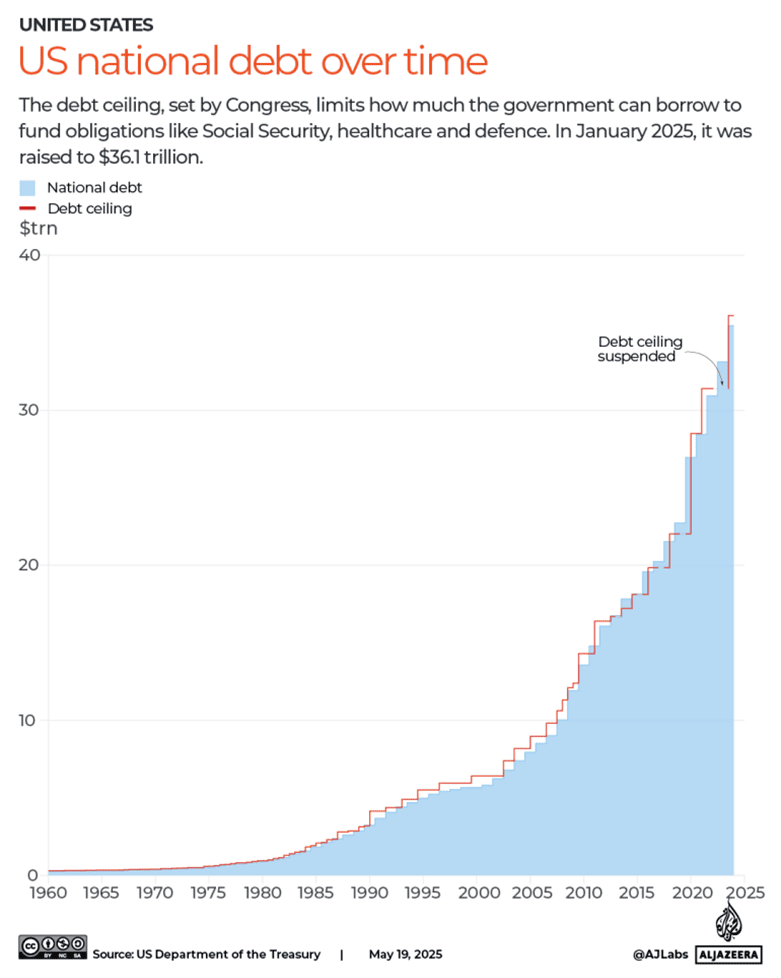

The U.S. Debt Clock website is not a light read with your morning coffee. While the site resembles a carnival ticketing center - colorful, with numbers increasing (not decreasing) in real-time - the reality is absolutely apocalyptic.1 Total U.S. national debt is in the $36 to $37 trillion range, which equates to approximately $108,000 per citizen and $323,000 per taxpayer.

Source: Federal Reserve Bank of St. Louis. June 3, 2025. “Federal Debt: Total Public Debt.”

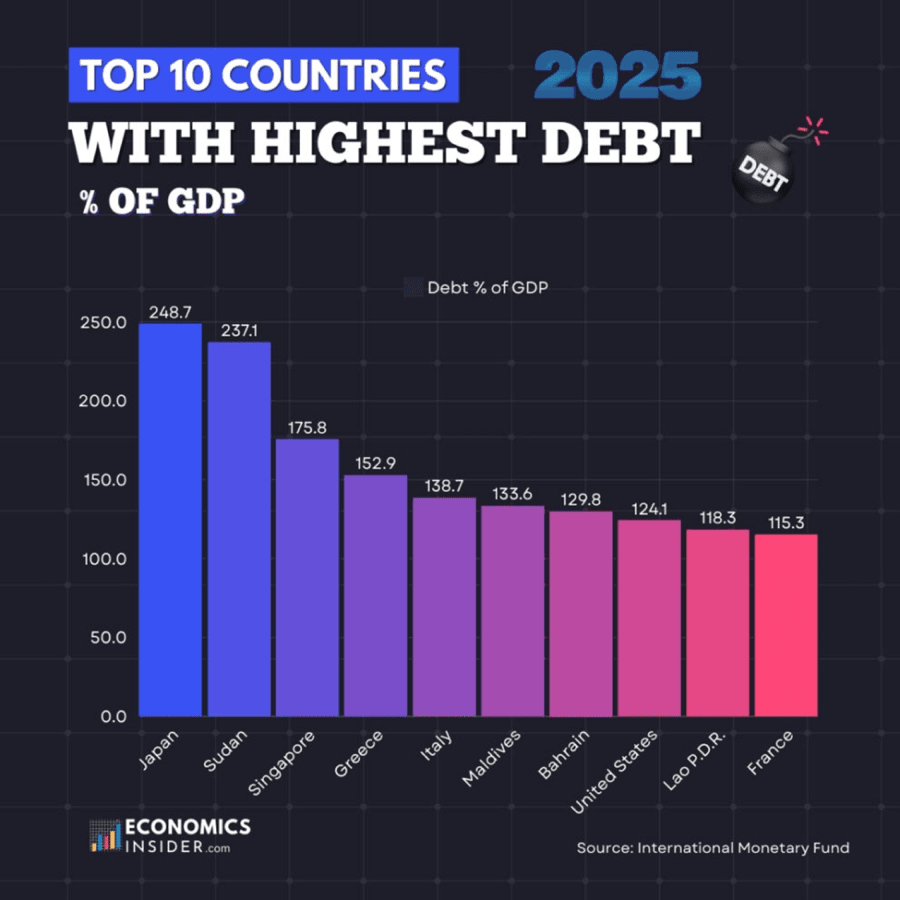

U.S. debt-to-gross domestic product (GDP) was a manageable 34% in 1980, skyrocketed to 57% by 2000, and is now 124%. If this sounds unworkable, it very well might be. Yet, one of the most important questions is not the country’s debt-to-GDP ratio, but compared to whom.

Source: Economics Insider. December 21, 2024. “Top 10 Countries With Highest Debt-to-GDP Ratio in 2025.”

A quick review of the chart reveals that seven developed countries are among the Top 10. Japan is one of the most advanced nations on the planet, and as any tourist to Tokyo would tell you, there’s nothing in the air that screams a 248% debt-to-GDP ratio.

Nevertheless, this is the central problem. Most everyday people don’t feel the debt, or at least don’t perceive their daily struggles to be associated with elevated debt levels. In parallel, when politicians do speak in earnest about addressing the debt, taxation and entitlement cuts places them in unfavorable positions with the broader electorate.

Annual Deficits Add Up

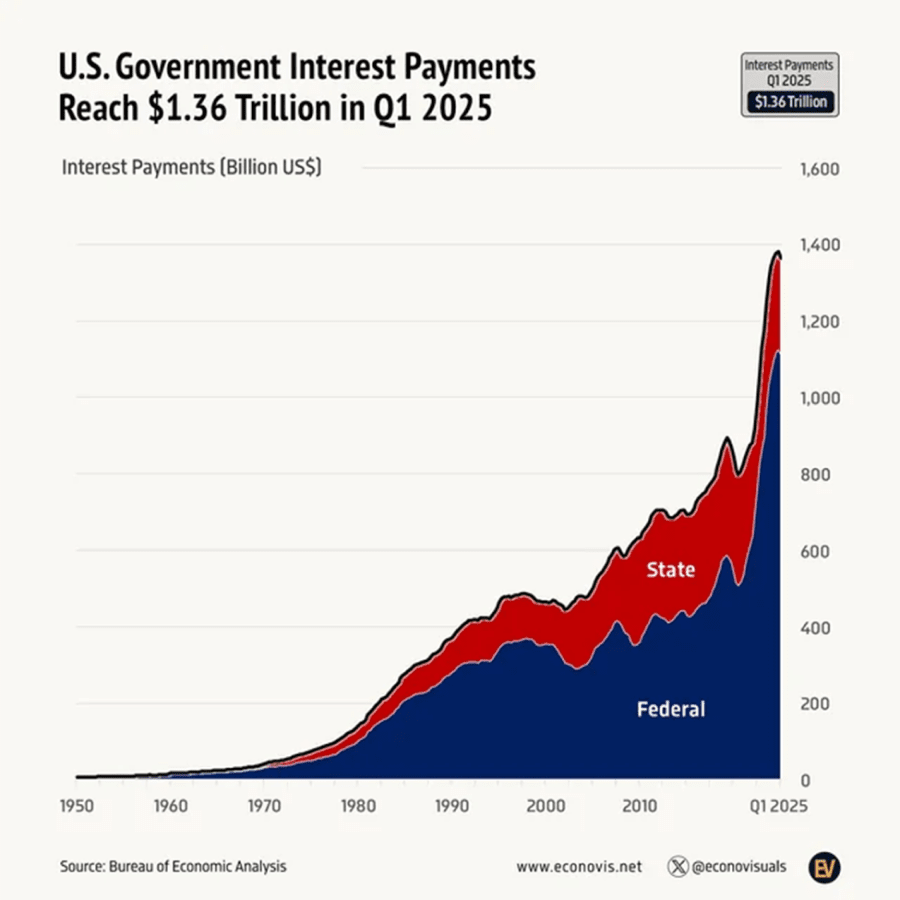

Debt of any kind constrains the holder from investing current or future revenue in constructive activities. The holder has borrowed to pay for things in the short term, and the cost of that borrowing arrives in the form of interest payments. Depending on the amount borrowed and the payment terms, the interest payments may be worthwhile. But the U.S. now pays more in interest payments than it pays to fund the country’s defense.

To put $1.36 trillion in interest payments into context, the U.S. spends $907 billion on defense, $1.5 trillion on Social Security, and $1.6 trillion on Medicare and Medicaid.2 The great historian, Niall Ferguson, remarked last year:

“Any great power that spends more on debt service (interest payments on the national debt) than on defense will not stay great for very long. True of Habsburg Spain, true of ancien régime France, true of the Ottoman Empire, true of the British Empire, this law is about to be put to the test by the U.S. beginning this very year.” 3

While the British example is a cautionary tale, the U.S. has a couple of things going for itself. The country’s greatest asset is arguably its currency. The dollar faces few rivals, and to better understand its strength, researchers from New York University and the Federal Reserve Board employed a valuation model based on two decades of data from the International Monetary Fund. Their findings concluded that the dollar’s dominance comes from:4

- Global Savings

- Investor Demand

The U.S. can borrow and add to its debt because the full faith and credit of the United States government backs U.S. Treasury bills, notes, and bonds. The country has never defaulted on its debt, which makes any of the following safe, stable, and predictable for investors:

- Treasury (T) Bills - Mature within one year

- T Notes - Mature between 2 and 10 years

- T Bonds - Mature in 20 to 30 years

The Treasury market has behaved erratically since “Liberation Day,” but one of the best arguments for the dollar is that an alternative is not entirely clear. The Euro, Pound, and Yen are the closest alternatives, but the U.S. eclipses all three for two reasons:

- Size - The U.S. is the world’s largest economy (by a lot), with the dollar representing 57% of global foreign exchange reserves and 88% of foreign exchange transactions.5

- Competitiveness - Home to the largest stock, real estate, and bond markets, an impressive 46% of global GDP is pegged to the dollar.

The dollar saw its value decline by nearly 10% over the first half of the year.6 That’s certainly a drop, and one that has added to recent noise surrounding whether the currency can maintain its dominance. Alternative investments provide some shelter, but the dollar’s reserve status is not something the U.S. can afford to lose.

Role of Stablecoins

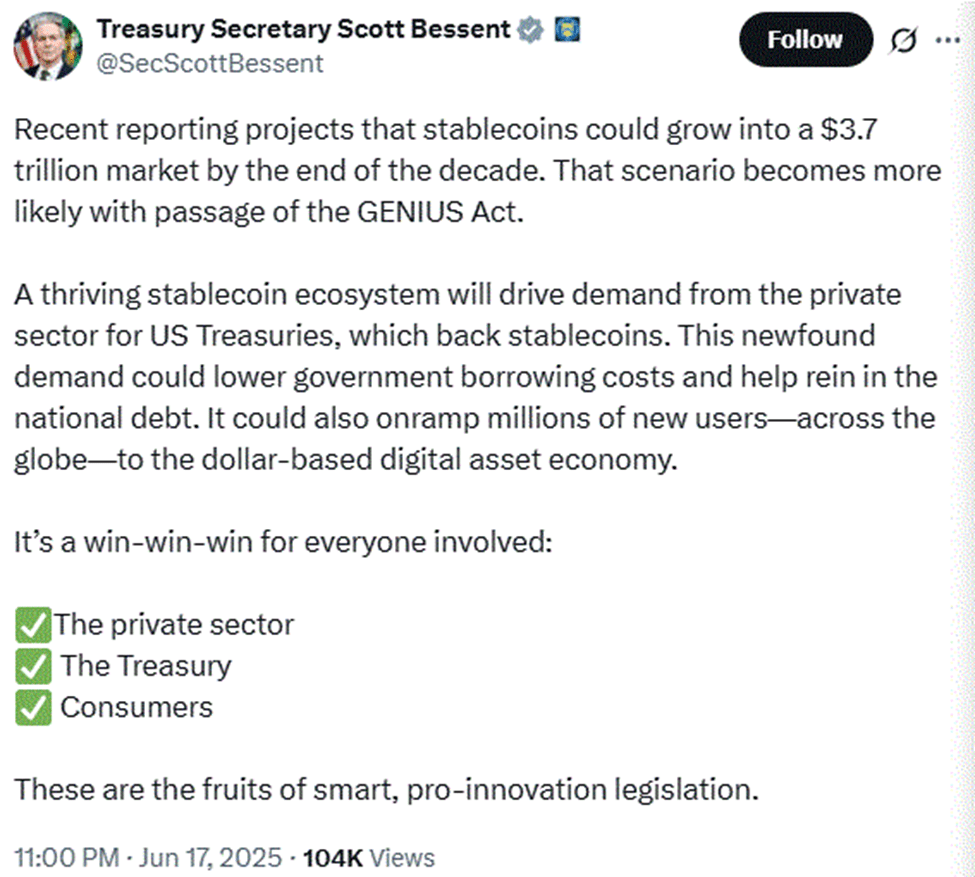

Dollar dominance, long term, is one way to ensure the entire empire doesn’t come crashing down. On June 17, the Senate passed legislation to establish a regulatory framework for stablecoins.7 Pegged to assets such as the dollar or gold, the overall stablecoin market is valued at roughly $255 billion. A staunch supporter, Treasury Secretary Scott Bessent revealed his thoughts on X:

Source: Treasury Secretary Scott Bessent X Account.

Stablecoins are popular internationally due to their relatively low cost and quick transactions. Moreover, in emerging markets with large “unbanked” populations, stablecoins provide a viable alternative to traditional financing.9 If global demand continues to increase, the U.S. could essentially construct a “financial moat” around the dollar, thereby increasing its position as the global reserve currency.10

The Options on the Table

If you owe a creditor $10,000 and need to pay down that debt, you can:

- Cut expenses

- Make more money

- Or employ a combination of the two

Cutting expenses is important, but meaningful cuts would only be made in the areas previously mentioned - Social Security, Medicare/Medicaid, and defense. To the President’s credit, he has expressed a desire to negotiate with China, Russia, and others to engage in coordinated defense spending cuts. Regarding Social Security and Medicare/Medicaid, the electorate is still not in a position to support a mature conversation, unfortunately.

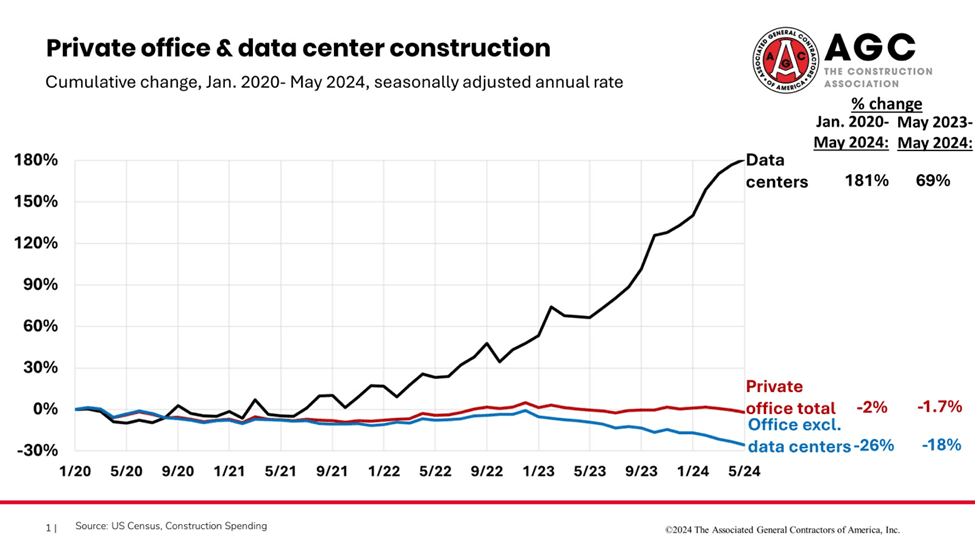

Growing our way out of debt is a more nuanced process. The U.S. has the world’s deepest capital markets. Approximately $23 trillion is parked in U.S. money markets and deposits,11 and in a scenario with lower interest rates, investors would allow that money to circulate into growth-generating assets. The infrastructure sector is a rapidly growing private market, and artificial intelligence (AI)- driven data center construction could be a significant growth driver that expands the economy, ultimately at a rate of 3 to 4% annually.12

Railroad expansion between 1860 and 1890 accounted for 25% of the increase in U.S. GDP.13 Between 1950 and 1989, investments in the country’s interstate system spearheaded a quarter of productivity growth.14 Data center construction would spur employment, leverage private and public sector funding, and, most importantly, help the country make a meaningful dent in its debt.

Conclusion

The $36 trillion ton elephant in the room is now out in the open for everyone to see. Further “can kicking” down the road will ultimately shoulder the youngest among us with an unmanageable debt bill. Addressing expenses, maintaining the dollar as the principal reserve currency, and making meaningful investments to grow the economy so that the debt-to-GDP ratio either stabilizes or declines are the challenges we face. A polarized political environment stands in the way.

Sources:

- US Debt Clock

- Ibid

- Seib, Gerald F. June 21, 2024. “Will Debt Sink the American Empire?” The Wall Street Journal.

- Ibid

- Atlantic Council. “Dollar Dominance Monitoring.”

- Pavlus, John. June 16, 2025. “What Makes the U.S. Dollar So Special?” KelloggInsight.

- Neukam, Stephen. June 17, 2025. “Senate passes GENIUS Act despite crypto corruption concerns.” Axios.

- AInvest. June 17, 2025. “Stablecoins Could Reduce U.S. National Debt by 2030, Says Treasury Secretary.”

- Lequier, Lucie. June 17, 2025. “Why Stablecoins Are Gaining Popularity.” Barron’s.

- Aziz, Ayesha. April 6, 2025. “Web3 CEO Says Stablecoins Are Key To Ensuring U.S. Dollar Dominance in Global Markets.” Yahoo Finance.

- Federal Reserve Bank of St. Louis. June 13, 2025. “Deposits, All Commercial Banks.”

- Fink, Larry. November 5, 2024. “How to Grow Out of America’s Debt Woes.” The Wall Street Journal.

- Ibid

- Phelps, Hailey. Second/Third Quarter 2021. “When Interstates Paved the Way.” Federal Reserve Bank of Richmond.