Alternative Investments for Retirement

Alternative Investments for Retirement

By: Peter Frerichs

August 25, 2025

Insight Highlights

- Differentiate your practice: Stand out by offering solutions beyond the traditional menu.

- Enhance retirement outcomes: Alternatives can help smooth returns and mitigate volatility.

- Institutional-quality access: Provide clients with professionally sourced, vetted managers typically unavailable in standard retirement plans.

President Trump signed an executive order that sets the stage for the incorporation of alternative, private investments in retirement plans. While the notion of more, as opposed to fewer, options for fund holders seems logical, there is considerable noise surrounding the addition of alternative investments for retirement. The arguments come from a rational space, but two propositions warrant more thoughtful consideration:

- American retirement savings are in desperate need of a kickstart.

- The alternative investment space in 2025 has evolved considerably.

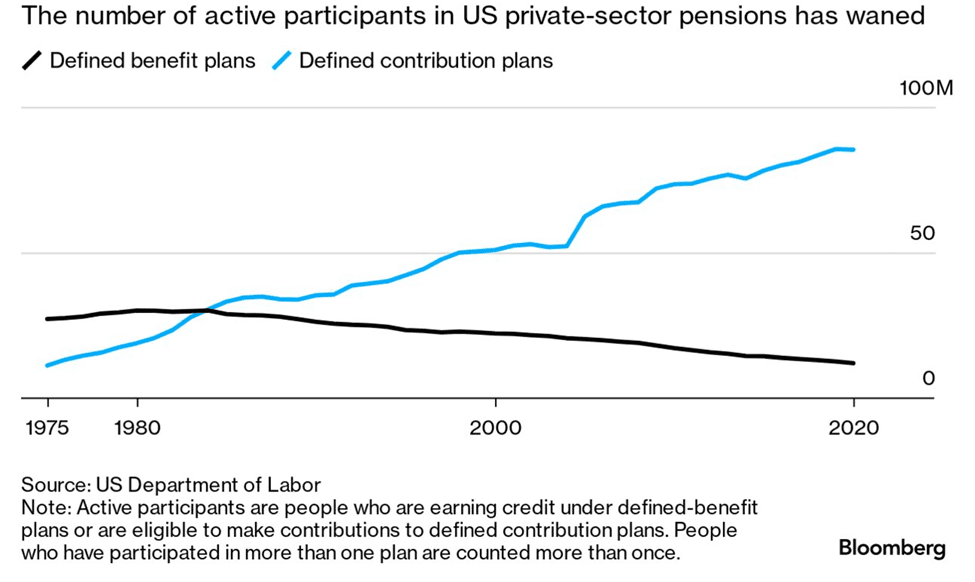

A Relic of the Past - Employer-Defined Benefit Plans

Decline of Pensions, Rise of 401(k)s

During the early 2000s, high-profile bankruptcies in the airline industry uncovered staggering pension liabilities. United and U.S. Airways had to collectively terminate and transfer $9.7 billion to the Pension Benefit Guaranty Corporation (PBGC), and plan participants ultimately lost $5.3 billion in benefits.1 With the exception of the public sector, defined benefit plans have been on the decline since the mid 1970s. Defined contribution plans, 401(k)s being the most popular, have taken off, but they were never designed to be a long-term substitute.

401(k)s Need More Options

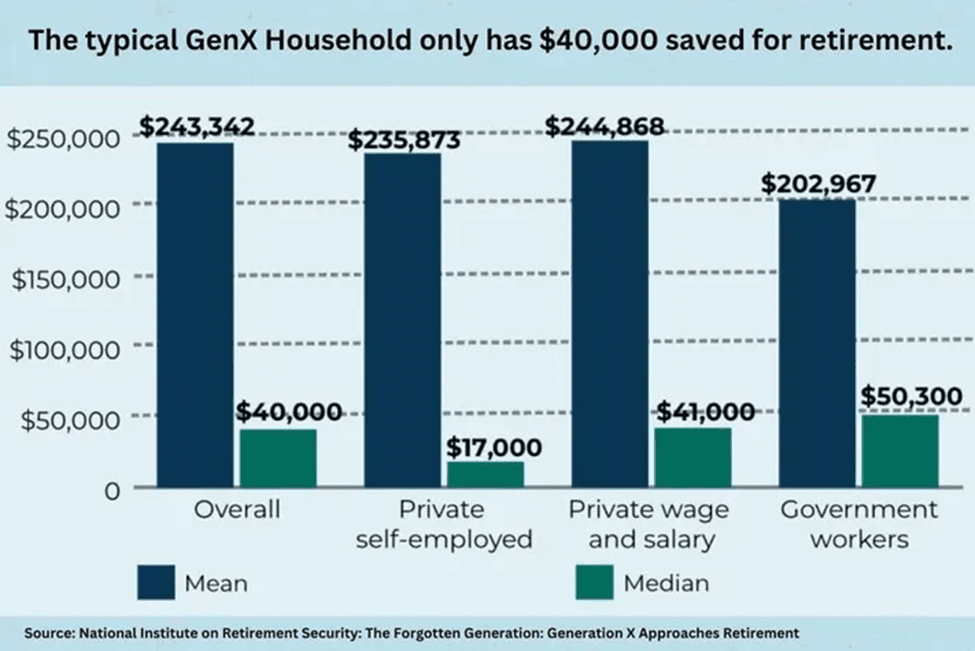

"The retirement savings crisis in the United States is no longer looming: it is here now."2

— National Institute on Retirement Security, 2024

The retirement savings crisis is multifaceted. The quick and dirty reality, however, is that it’s here, and in the words of BlackRock CEO, Larry Fink, in his recent annual letter, “We’re going to need better ways to boost portfolios.”3

The elder members of Generation X (those born between 1965 and 1980) are approaching retirement age, and the median Gen X household only has $40,000 in retirement savings.4 This is the first generation to enter the workforce after the shift away from defined benefit pensions. A handful of economic crises and sluggish wage growth have taken their toll on portfolios, and while alternative investments for retirement won’t solve the crisis on their own, the potential upside should not be ignored.

President Trump’s Executive Order

The President’s executive order directs the Secretary of Labor to assess fiduciary guidance on alternative investments for retirement in 401(k)s and similar plans. Private equity is already offered in some 401(k)s, but according to the 2024 DC PLANSPONSOR Benchmarking Report, representation amounts to only 2.2% of plans.5

The President’s order rests on two points:

- Since its peak in the 1990s, the number of publicly listed US companies has declined by approximately 50%.6

- Companies are remaining private for longer, leaving public investors on the outside looking in.

By providing alternative investments for retirement, the Administration is seeking to widen the menu of investment opportunities for everyday Americans.

Arguments for Alternative Investments for Retirement

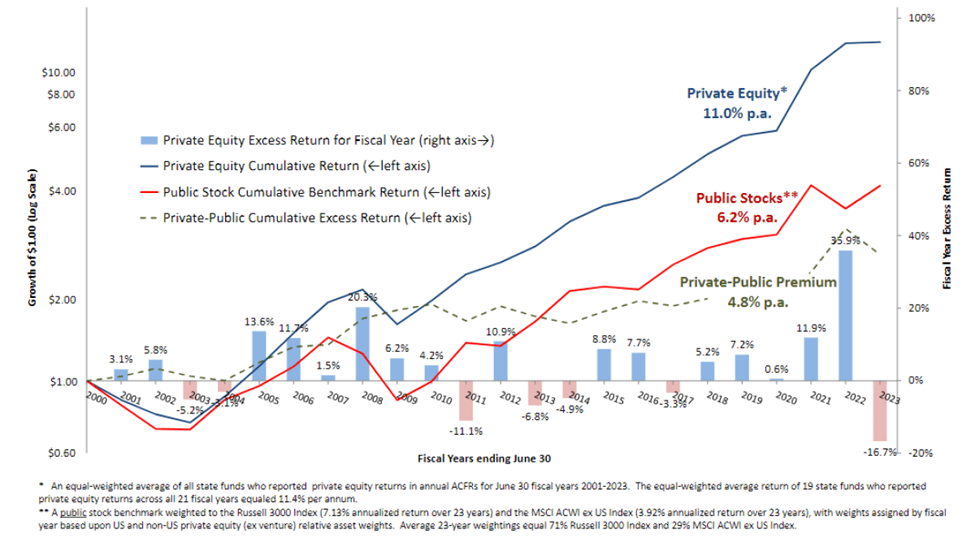

Some of the country’s largest public pension funds have been traditionally bullish on alternative investments. As of June 2023, the California Public Employees Retirement System led the nation with $60.15 billion in private equity investments, followed by the California State Teachers Retirement System with $48.95, and the Washington State Investment Board with $44.90.7

Composite Private Equity Performance across State Pensions:

Covering 23 Years starting June 30, 2000, and ending June 30, 2023 Growth of $1.00 (left axis) and Annual Excess Return (right axis)

Alternative investments for retirement, such as infrastructure and real estate, protect investors during market downturns, the principal reason pension funds have invested in these positions for decades. University endowments follow a similar investment strategy, and overall pension funds outperform 401(k)s by roughly 0.5% each year.8

Second, the public is clamoring for change. A January survey by the national polling firm Fabrizio Ward found that voters supported reforming regulations to allow private equity fund options through their 401(k) plans by a 57% - 13% margin.9 Moreover, 64% believed it was unfair that only institutional and wealthy investors had access to alternative investments for retirement.10

Movement is on the horizon with some notable partnerships already in the works:

- Empower, the second largest retirement plan provider in the country, teamed up with Goldman Sachs, Apollo, PIMCO, Sagard, Partners Group, Neuberger Berman, and Franklin Templeton to offer its 19 million clients access to alternative investments for retirement. CEO, Ed Murphy, points out that, “Right now, 87% of companies in the U.S. with revenues over $100 million are private.”11

- Voya Financial, Inc. holds $630 billion plus in defined contribution assets for over 9 million plan participants. A new partnership with the alternative asset manager, Blue Owl Capital, Inc. will provide private, alternative investments for retirement through advisor-managed accounts on the Voya platform.12

- The State Street Target Retirement IndexPlus Strategy is a new offering from State Street Global Advisors. Target allocations will follow a 90% exposure to public markets and 10% to private markets.13

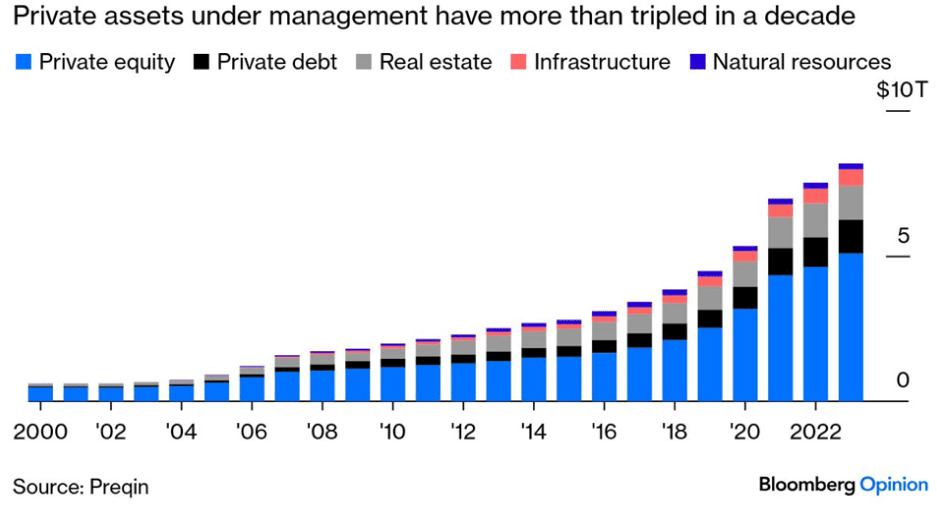

An Established Industry

Private assets under management have grown exponentially over the past twenty years.

A Growing Alternative to Public Markets

Source: The Editorial Board. February 7, 2025. “Private Equity and 401(k)s Aren’t a Great Match.” Bloomberg.

While concerns around transparency are valid, Empower CEO Murphy noted in his response to Senator Warren that Empower has already embarked on plans for fiduciary accountability and participant protection. For example, Empower retirement plan participants can only access alternative investments for retirement if their employers have examined the investments under the Employee Retirement Income Security Act (ERISA)’s fiduciary standards.14

Regarding lock-ups, it is true that private investments do typically feature longer lock-up periods. Yet, the overwhelming majority of investments in an everyday 401(k) are liquid assets, where alternative investments for retirement would only represent a fixed percentage, which ultimately behaves according to the risk profile of the account holder. Semi-liquid strategies, such as interval funds, already exist and offer periodic, quarterly repurchase windows.

A Critic’s Take on Alternative Investments for Retirement

Critics of alternative investments for retirement frequently cite two concerns:

- Transparency

In mid-June, Senator Elizabeth Warren (D-MA) penned a letter to Empower CEO Ed Murphy surrounding the company’s inclusion of alternative investments for retirement in 401(k)s and similar plans. Senator Warren referenced the oversight role of the Securities and Exchange Commission (SEC) with publicly traded companies and a lack of a similar body for private companies.

- Lock-up Periods

In general, private equity investors are “locked in” for anywhere between 5 and 10 years, and sometimes more. The investment is longer-term in nature, and a worry on the critic’s side is that portfolio holders will lack access to immediate liquidity.

Concluding Thoughts

All investments incorporate some measure of risk. Defined-contribution plans like 401(k)s have exploded in popularity, but their returns to date will not be enough to fund many people through retirement. Alternative investments for retirement, responsibly managed and selected according to each individual’s risk appetite, can provide even more diversification and protection during downturns compared to the traditional retirement portfolio that the vast majority of Americans hold today. Implemented prudently, millions of people will soon have access to a suite of investment options that were once reserved for high-net-worth and major institutional investors.

Sources:

- U.S. Government Accountability Office. September 30, 2005. “Commercial Aviation: Bankruptcy and Pension Problems Are Symptoms of Underlying Structural Issues.”

- Bond, Tyler, Doonan, Dan, Kreps, Michael, Lowell, John, Price, Jonathan, and Wadia, Zorast. May 2024. “Policy Ideas For Boosting Defined Benefit Pensions in the Private Sector.” National Institute on Retirement Security.

- Burns, Tobias. July 31, 2025. “Access to 401(k)s couldn’t come at a better time for private equity.” The Hill.

- Doonan, Dan. April 11, 2024. “Americans Are Worried About Retirement Savings, And They Should Be.” Forbes.

- Van Bramer, James. July 18, 2025. “Ahead of Executive Order, What to Know About Private Equity in 401(k) Plans.” PLANSPONSOR.

- Murphy, Ed. July 7, 2025. “Letter to Senator Elizabeth Warren.” Empower.

- Light, Larry. July 22, 2024. “Private Equity Continues as Top Performer for Pension Plans, Study Says.” Chief Investment Officer.

- Burns, Tobias. July 31, 2025. “Access to 401(k)s couldn’t come at a better time for private equity.” The Hill.

- Pinpoint Policy Institute. “New Pinpoint Policy Institute Poll Shows Strong Support for Democratizing Investment Options in Workers’ 401(k) Plans.”

- Ibid.

- Sullivan, John. May 14, 2025. “Empower to Offer Private Investments in 401(k)s, CEO Ed Murphy Explains Why.” National Association of Plan Advisors.

- Voya Financial. July 14, 2025. “Blue Owl Capital and Voya Financial enter strategic partnership to bring private markets investments to defined contribution retirement plans.”

- PLANSPONSOR Staff. April 11, 2025. “Product & Service Launches.” PLANSPONSOR.

- Murphy, Ed. July 7, 2025. “Letter to Senator Elizabeth Warren.” Empower.

- Warren, Elizabeth. June 18, 2025. “Letter to Empower CEO, Ed Murphy.” United States Senate.